European Union (EU) proposals for changes to the over-the-counter (OTC) derivatives trading rules are underway. The final rules are not yet agreed, but we set out a summary of the proposals below. The changes will be relevant also to US and UK managers responsible for the European Market Infrastructure Regulation (EMIR) compliance of funds and investment vehicles under their management, and/or trading with EU counterparties.

A. EU proposal for EMIR 3

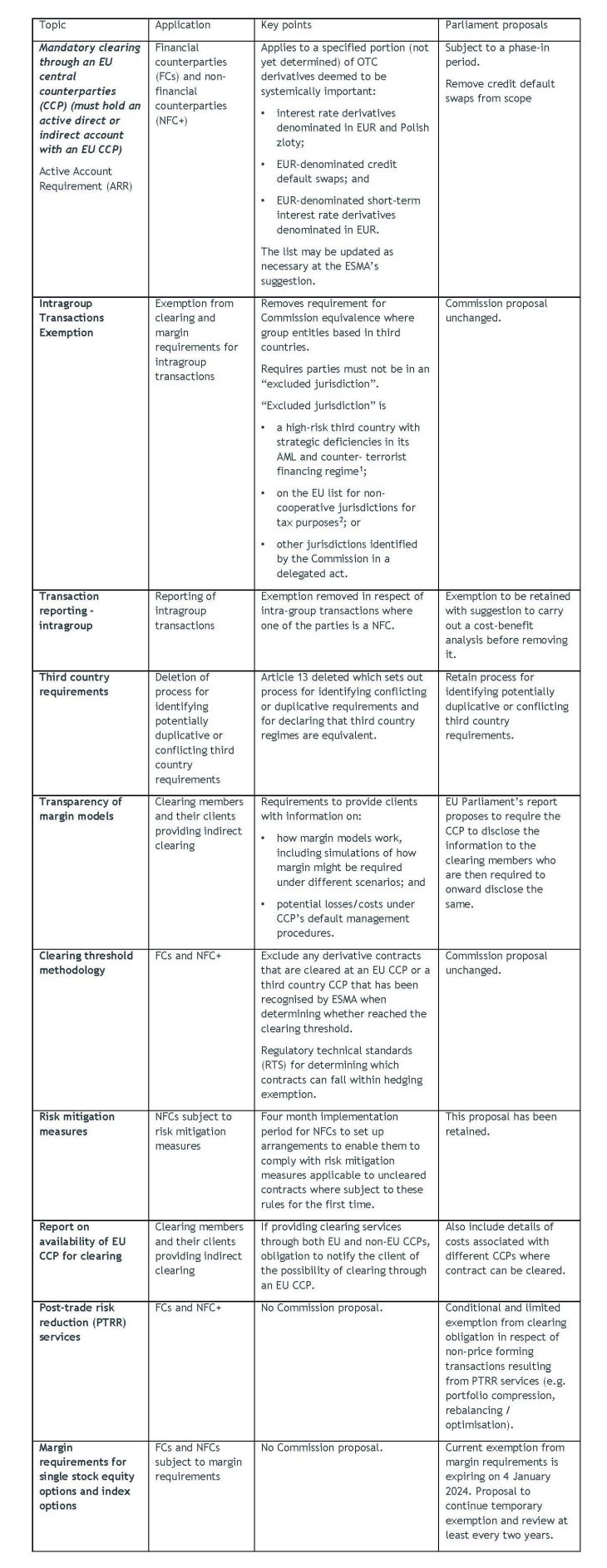

The key measures proposed by the EU Commission1, together with the EU Parliament's proposed changes2, include:

B. Industry Comments and Concerns

In between the Commission publishing its proposal and the EU Parliament responding with its set of proposed amendments, the International Swaps and Derivatives Association (ISDA) (together with the Alternative Investment Management Association (AIMA), European Fund and Asset Management Association (EFAMA) and the Futures Industry Association (FIA)) published a joint response5 to the Commission's proposals set out in EMIR 3. Some of the comments in the response were adopted in the Parliament's response (e.g. in respect of PTRR services, the exemption to the margin requirement for single stock equity options and index options, and reinstating the mechanism for reviewing third country regimes for potentially duplicative or conflicting requirements). However, some of ISDA's comments still apply.

In particular, there are areas that ISDA sees as harmful for the competitiveness of EU firms, including the active account requirement and proposals6to require firms to address concentration risk arising from CCPs as part of their Pillar 2 requirements.

While the response was broadly positive in respect of a number of the proposals, including in respect of removing the equivalence requirement from the intragroup transaction exemption, there was some concern regarding the proposals to require parties subject to the clearing obligation to hold an active account at an EU CCP and to clear a portion of certain derivatives through an EU CCP. The statement criticised the move as being anti-competitive and harmful to EU capital markets, affecting EU firms' ability to provide best execution to clients and imposing additional costs.

C. Next steps for EMIR 3

Now that the EU Parliament have introduced amendments to the Commission Proposal, the next stage of the legislative process will be for the Council to either accept the amended Proposal or amend further and send back to the Parliament for a further reading.

D. Divergence between UK and EU EMIR

The above changes, should they be implemented, would represent a divergence from the position under UK EMIR (unless the UK Government decides to implement similar changes).

Although the UK has largely implemented the changes to EMIR set out in REFIT and EMIR 2.2, there are some areas of divergence between the UK and the EU (in addition to the technical changes implemented as a result of the Brexit onshoring process). Some of the key changes under the UK Regime are set out below.

Financial Services and Markets Bill 2022/23 (the "FSM Bill")

The FSM Bill introduces a new power allowing the Bank of England to disapply the clearing obligation in respect of transactions resulting from PTRR services, in line with the ESMA recommendations mentioned above. The Bank of England's power will, however, be limited to circumstances where it considers its use necessary or expedient in the interests of financial stability. There may, therefore, be differences with the EU regime in respect of which transactions will be exempt from the clearing obligation.

Changes to EMIR Reporting Requirements

In February 2023, the FCA published its policy statement and final rules and guidance for changes to reporting requirements, procedures for data quality and registration of Trade Repositories7. Changes include amendments to the reportable fields in the UK EMIR technical standards.

These changes are due to take effect on 30 September 2024. To a large degree, the changes are consistent with changes that were made to EU EMIR reporting requirements and due to take effect in April 2024, as set out in new Guidelines8, with accompanying technical standards. However, the FCA did note that there are a small number of areas of divergence from the EU approach. The final versions of the UK EMIR Validation Rules and XML schemas are available on the FCA's UK EMIR reporting webpage9.

Changes to Margin Requirements for non-centrally cleared derivatives10

The key changes introduced by the amended rules include:

- Changes to the eligibility requirements for collateral meeting the margining requirements for non-centrally cleared derivatives in respect of units or shares in funds. Interests in third country funds / units in third country collective investment schemes will be eligible as long as they meet defined criteria11, have a daily public price quote and only invest in cash or securities that would themselves constitute eligible collateral. Firms must have carried out a risk assessment on the risk management protections under the relevant jurisdiction's legal framework.

- Where firms come under the margin requirements for the first time and the rules would otherwise apply immediately, the PRA and FCA have introduced a transitional period. This is 12 months where a firm comes into scope as a result of a change in the netting status of a jurisdiction. For all other circumstances where the margin requirements would otherwise apply immediately, the transitional period is six months.

In line with similar moves by the EU (as described above),the FCA and PRA are also consulting on further amendments to the margin requirements12to extend the temporary exemption for single-stock equity options and index options from the margin requirements for non-centrally cleared derivatives. The temporary exemption is proposed to be extended to 4 January 2026 to enable proper consideration of the right model for the final regime.

Footnotes

2. Published on 13 June 2023, https://www.europarl.europa.eu/doceo/document/ECON-PR-749908_EN.pdf

3. Pursuant to Article 9 Directive (EU) 2015/849 – the latest version of this list is available here: https://ec.europa.eu/transparency/documents-register/detail?ref=C(2022)9649⟨=en

4. https://www.consilium.europa.eu/en/policies/eu-list-of-non-cooperative-jurisdictions/

5. https://www.isda.org/2023/02/02/isda-comments-on-emir-3-package/ and https://www.isda.org/a/a6ygE/ISDA-commentary-EMIR-3.pdf

6. Included in the EMIR 3 proposals as amendments to the Capital Requirements Directive (Directive 2013/36/EU) and the Investment Firm Directive (Directive (EU) 2019/2034)

7. https://www.fca.org.uk/publication/policy/ps23-2.pdf

9. https://www.fca.org.uk/markets/uk-emir/reporting-obligation

10. Changes to the BTS 2016/2251 were made in final rules published by the FCA and PRA in Policy Statement PS11/22 on margin requirements for non-centrally cleared derivatives on 15 December 2022 (https://www.bankofengland.co.uk/prudential-regulation/publication/2022/december/margining-requirements-for-non-centrally-cleared-derivatives).

11. Set out in Article 7(2)(b) of the Large Exposures (CRR) part and Article 132(3) of the Standardised Approach and Internal Ratings Based Approach to Credit Risk (CRR) parts of the PRA Rulebook.

12. https://www.bankofengland.co.uk/prudential-regulation/publication/2023/july/margin-requirements-for-non-centrally-cleared-derivatives

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.