Welcome to the Student Lending chapter of our annual report Consumer Financial Services 2023 Year in Review.

Looking Ahead to 2024

The CFPB will likely continue to focus on junk fees, nontransparent and other "illegal" practices relating to student loan servicing, and the hidden costs of college tuition payment plans.

Key Trends From 2023

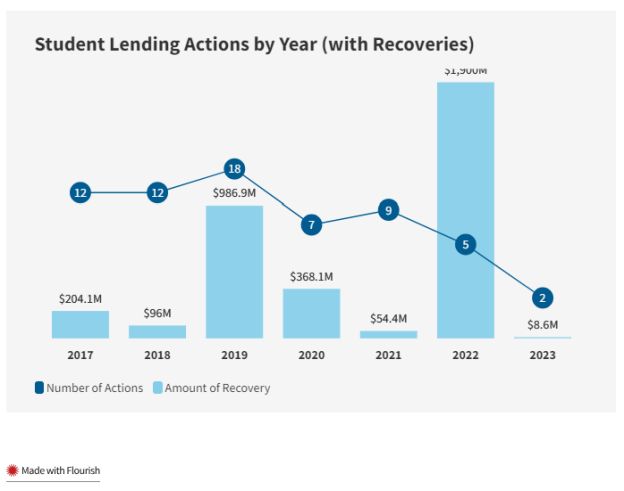

In 2023, Goodwin tracked only two enforcement actions related to student lending, a decrease from the five actions Goodwin tracked in 2022. These actions resulted in total recoveries of approximately $8.6 million, a marked decrease from the $1.9 billion in recoveries in 2022 and $55 million in 2021. States also took on a robust role in ensuring compliance by student loan servicers in 2023, with several states recently tightening their controls around student lending, including California, Connecticut, and Maine, as described in more detail below.

In the News

In March, the CFPB issued a bulletin advising student loan servicers to remain aware and faithful to their obligation, which the CFPB described in a news release as "to halt unlawful conduct with respect to private student loans that have been discharged by bankruptcy courts." The bulletin noted that even though some student loans are subject to an "undue hardship" standard that requires a separate proceeding to discharge them, some private student loans can be, and are, extinguished in a standard bankruptcy proceeding. Examples of student loans eligible for discharge via a standard bankruptcy proceeding, as provided in the bulletin, include (1) loans to students attending school less than half-time; (2) loans made in amounts in excess of the cost of attendance, which are often disbursed directly to the borrower instead of the school; (3) loans made to cover fees and living expenses incurred while studying for the bar exam or other professional exams; and (4) loans made to cover fees, living expenses, and moving costs associated with medical or dental residency. The CFPB's bulletin described the Bureau's finding that even when a student loan was discharged in a standard bankruptcy proceeding, student borrowers who continued to receive collection notices from loan servicers often continued to make payments.

2023 Enforcement Highlights

CFPB Teams Up With 11 States to Bring Enforcement Action Against Delaware-Based Company Prehired Over Income-Share Loan Program

In November, the CFPB announced that as a result of an enforcement action it brought alongside 11 states (Washington, Delaware, California, Oregon, Minnesota, Illinois, South Carolina, North Carolina, Massachusetts, Virginia, and Wisconsin), Delaware-based company Prehired would pay more than $30 million in relief to student borrowers. The company operated a 12-week online training program claiming to prepare students for entry-level positions as software sales development representatives and allegedly engaged in "abusive" debt-collection practices as part of its income-share loan program.

The lawsuit, which was filed in July 2023, alleged that Prehired had (1) deceived borrowers by claiming its loans were not in fact loans, (2) concealed loan information from borrowers, (3) tricked consumers by employing deceptive debt-collection practices, and (4) sued students in a distant location when they did not make timely or complete payments. According to Director Chopra, "Prehired lured student borrowers into debt with false promises of job placements and claims that students wouldn't have to pay until they got a job." The proposed stipulated final judgment and order provides that Prehired will (1) refund $4.2 million to student borrowers, (2) cancel all outstanding income-share loans, (3) shut down permanently, and (4) pay a nominal civil money penalty.

FTC Files Lawsuit Against For-Profit College Over Allegedly False Advertising and Its Income-Share Loan Program

In October, the FTC sued for-profit school Sollers College and its parent company, Sollers Inc., alleging that "the companies lured prospective students to enroll by falsely touting their job-placement rates and that their relationships with prominent companies would lead to jobs after students graduate." The complaint also accused Sollers College of encouraging students to sign "income share agreements" to pay for the school. These types of agreements "require students to pay the school a percentage of their future income in exchange for covering their tuition." According to the FTC, certain borrowers' rights were left out of the income-share agreements. Further, the FTC alleged that Sollers College "falsely advertise[d]" its relationships with potential employers when in reality, the school had no such relationships. These allegations were resolved in a stipulated order issued in October. Pursuant to the stipulated order, Sollers agreed to (1) stop collecting debts from students on any income-share agreements it currently holds, (2) repurchase any income-share agreements it sold to third parties to stop collection efforts on those agreements, (3) request that consumer reporting agencies delete the debt from consumers' credit reports, and (4) provide written notification to consumers who are receiving debt forgiveness under the proposed order.

Click to access all 12 chapters of our Consumer Financial Services 2023 Year in Review, including a market overview about the industry overall and chapters on 11 industry segments.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.