As of January 1, 2024, reporting requirements under the federal Corporate Transparency Act and related regulations (collectively, the "CTA") went into effect. The CTA creates a new reporting requirement for many small, private companies as part of the U.S. government's efforts to make it harder for bad actors to hide or benefit from their ill-gotten gains. While the purpose is laudable — to stop money launderers, terrorists, and other law breakers — the new reporting requirement creates new and ongoing compliance obligations that will require action for many small businesses.

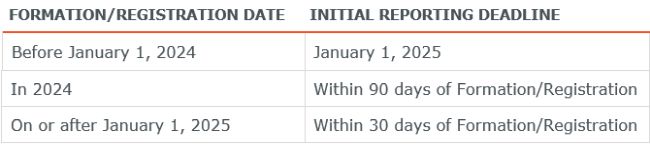

Fortunately, the CTA allows a cushion for filing initial reports for many reporting entities. Each non-exempt "reporting entity" (discussed below) must meet the following deadlines for its initial filing:

The following article highlights the types of entities that must report under the CTA, the types of entities that are exempt, what information must be reported, where additional information can be found, and certain other information about the CTA.

Which Entities Must Report?

The CTA imposes reporting obligations on most corporations, LLCs, and other entities created by the filing of a document with a secretary of state or any similar office in the U.S. (including territories and possessions) or with an Indian tribe, and foreign companies registered to do business in any jurisdiction in the U.S. or with any Indian tribe. Accordingly, unless an exemption applies, all corporations, LLCs, and other entities formed or registered in the U.S. will need to file, even in cases where the entity has limited operations or one or only a few owners.

Which Entities Are Exempt?

The CTA expressly excludes 23 categories of entities from the reporting requirements. One of the most commonly applicable exemptions is for "large operating companies," which are entities (1) with more than 20 full-time employees in the U.S.; (2) that have an "operating presence" at a physical office in the U.S.; and (3) which reported over $5 million in gross receipts or sales on its filed prior year federal tax return (net of returns and allowances, and with gross receipts or sales from outside the U.S. excluded; note, however, if the entity is part of an affiliated group of corporations, it may be able to use the consolidated return in reaching this threshold). Additionally, while subsidiaries of certain other exempt entities are also exempt, please note that reporting entities whose ownership is controlled or wholly owned, directly or indirectly, by an exempt large operating company will also be exempt.

Here is the list of exemptions available under the CTA:

The specific criteria for each exemption are set forth in FinCEN's guidance materials — see below. Notably, the criteria for any specific exemption may have multiple components that must be met to qualify. Attention to detail will matter.

What Information Must Be Reported?

A reporting entity must submit a beneficial ownership information ("BOI") report to the U.S. Treasury's Financial Crimes Enforcement Network ("FinCEN"). The BOI report must disclose information about the reporting entity itself, its beneficial owners (a term more broadly interpreted than the designation implies; see below), and, in the case of an entity created or registered on or after January 1, 2024, its "company applicants." Note that beneficial ownership and company applicant information must be for individual and not upstream entity owners.

With respect to the reporting entity, the BOI report must include the entity's:

- Full legal name;

- Any trade names (including doing business as (d/b/a) and trading as (t/a) names);

- Complete current U.S. address;

- State, tribal, or foreign jurisdiction of formation;

- For a foreign reporting company, the state or tribal jurisdiction of its first registration in the U.S.; and

- IRS taxpayer identification number, including employer identification number (if it has no U.S. TIN, a foreign reporting entity can provide the tax identification number issued by the relevant foreign jurisdiction together with the applicable jurisdiction).

With respect to beneficial owners and company applicants, the BOI report must include the individual's:

- Full legal name;

- Date of birth;

- Complete current (home) address (although company applicants who do that work in the ordinary course of business may use the business address); and

- Unique identifying number from any of the following nonexpired identification documents issued to the individual: (a) U.S. passport; (b) driver's license; (c) a state, local government, or Indian tribal issued identification document; or (d) foreign passport if an individual lacks any of the above documents. An image of the identification document must also be provided.

As noted, if the reporting entity was created or registered on or after January 1, 2024, then it must also disclose its company applicant(s), defined as an individual who either: (1) directly files the document that creates a domestic reporting entity or first registers a foreign entity to do business in the U.S.; and/or (2) is primarily responsible for directing or controlling the filing of the relevant document by another, if more than one individual is involved in the filing. Each newly formed reporting entity must have at least one or at most two company applicants.

FinCEN ID Alternative. If a beneficial owner or company applicant would prefer to provide reportable information directly to FinCEN, the individual may obtain a FinCEN identifier ("FinCEN ID") by providing to FinCEN the same information that the reporting entity is required to provide. The reporting entity may then report the individual's FinCEN ID on its BOI report in lieu of listing the specific information described above regarding the individual. We expect individuals who have ownership stakes in numerous entities, or who regularly organize entities, may choose to take advantage of this alternative.

Who Is a Beneficial Owner?

A "beneficial owner" includes any natural person who directly or indirectly: (1) exercises "substantial control" over the reporting entity; or (2) owns or controls 25% or more of the ownership interests of the reporting entity. The term "substantial control" under the CTA is expansive and not necessarily the same as the concept of control under other federal statutes, including the federal securities laws. The CTA is explicit that senior officers, such as the company's president, chief financial officer, general counsel, chief executive officer, and chief operating officer, if any, all exercise substantial control, and provides other examples where an individual may directly or indirectly exercise substantial control over a reporting entity. A reporting entity must carefully review FinCEN's guidance materials or seek counsel to determine the scope of individuals who qualify as "beneficial owners" for reporting purposes.

When Must the Report Be Filed?

The initial filing deadlines are set forth in the introductory paragraphs of this article. There are no annual filing requirements thereafter, but any changes or corrections must be filed promptly. You must keep in mind that filing under the CTA is an ongoing requirement; it is not a "one and done" filing.

A reporting entity has 30 days to report any change to the information in its BOI report regarding the reporting entity or its beneficial owners. For example, a change in a beneficial owner's home address must be reported within 30 days. There is no materiality threshold regarding a reporting entity's obligation to report changes to any required BOI report information; the reporting entity must report all changes to the required information. Also, if the reporting entity becomes aware or has reason to know that any information in its previously filed BOI report was inaccurate when filed, it must file a correction within 30 days to correct any and all inaccuracies.

Who Has Access to Reported Information?

Information filed pursuant to the CTA, including the BOI report, will not be available in a database available to the public. Rather, FinCEN is required to store BOI in a secure non-public database (referred to as BOSS). As of February 20, 2024, FinCEN may disclose the reported BOI only upon receipt of a request, made through appropriate protocols, by: (1) U.S. federal agencies engaged in national security, intelligence, or law enforcement activities, for use in furtherance of those activities; (2) a state, local, or tribal law enforcement agency, if a court of competent jurisdiction has authorized the law enforcement agency to seek the information in a criminal or civil investigation; (3) a federal agency on behalf of non-U.S. law enforcement or a foreign prosecutor or judge; and (4) officers and employees of the Treasury Department for tax purposes. At some future date when additional regulations are finalized, FinCEN will also be able to disclose certain reported BOI to (a) a financial institution, with the consent of the reporting entity, to facilitate the financial institution's compliance with customer due diligence requirements under applicable law; and (b) federal and state regulators assessing financial institutions for compliance with legally required customer due diligence obligations. This could replace some of businesses' "know your customer" duties in opening accounts or borrowing.

What Are the Penalties for Violation?

The CTA provides for civil and criminal penalties for violations, including (1) a civil penalty of up to $500 per day; and, (2) a fine of up to $10,000, imprisonment for up to two years, or both, for any person who willfully: (a) provides or attempts to provide false or fraudulent BOI; or (b) fails to report complete or updated BOI to FinCEN. Penalties may also apply to reporting entities and individuals who (1) cause a reporting entity not to report; or (2) are senior officers of a reporting entity at the time of its failure to fulfill its obligation to accurately report or update BOI. Accordingly, businesses required to report should take the new reporting requirements seriously and take the necessary steps to fully comply and update as required.

Where Can Additional Materials Be Found?

FinCEN has published and regularly updates answers to certain FAQs it has received regarding the reporting requirements, which can be found here. FinCEN has also published a Small Entity Compliance Guide, which can be found here. We encourage you to carefully review the FinCEN materials to determine the applicability of the CTA and its reporting obligations to your entities or groups of entities.

What Should You Do Next?

For many businesses with simple ownership and control structures, it will be easy to comply with the new reporting requirement under the CTA. In fact, FinCEN has stated that it expects that many, if not most, reporting entities will be able to submit their BOI to FinCEN on their own using the guidance FinCEN has issued. As noted, we encourage you to review this guidance carefully since it contains considerable detail. Reporting entities are required to submit reports electronically through a filing system available on FinCEN's website here.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.