As previewed in last week's post, today the SEC held an Open Meeting to discuss its long-anticipated proposed amendments on climate-related disclosures. The proposal is now live here as is the Fact Sheet.

The proposed amendments would (1) add a new subpart to Regulation S-K that requires registrants disclose certain climate-related information in a separate section of their registration statement or annual report, and (2) add a new article to Regulation S-X that requires registrants include certain climate-related financial statement metrics and related disclosure in a note to their consolidated financial statements.

Key highlights of the proposed rule include mandates to disclose:

- Scope 1 and 2 emissions;

- Scope 3 emissions, if material, "or if the registrant has set a GHG emissions target or goal that includes Scope 3 emissions, in absolute terms, not including offsets, and in terms of intensity";

- Internal carbon prices, information about the price and how it is set, if a registrant uses an internal carbon price;

- Both physical and transition risks related to each line item of the consolidated financial statement, unless, as aggregated, the impact is below a materiality threshold of 1% of the total line item; and

- Information about a registrants publicly set climate-related targets or goals, including the scope of activities, how the registrant plans to meet its climate targets, relevant data to show the registrant is making progress, and if carbon offsets or renewable energy certificates are being used.

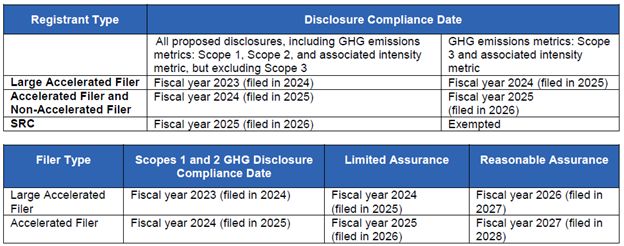

Importantly, the rule will phase-in for all registrants depending on the registrant's filer status, with a later phase-in period for Scope 3 emissions disclosures, see Table 1 below that assumes a December 2022 final rule. The proposed rule incorporates some of the concepts and vocabulary from the Task Force on Climate-Related Financial Disclosure and the Greenhouse Gas (GHG) Protocol, which are commonly used by companies in their sustainability and related reports. The GHG Protocol is also the foundational document for pending legislation in California (SB-260) on climate-related disclosures, as we discussed here. Lastly, the amendments include an exemption of Scope 3 emissions disclosure for small reporting companies and a safe harbor for Scope 3 emission disclosure (e.g., Scope 3 emissions disclosures will not be deemed fraudulent statements unless made without a reasonable basis or in bad faith).

The Commissioners' discussion of the rule at the Open Meeting illuminated sharp disagreement between Commissioner Hester Peirce who voted against the amendments and the other three Commissioners who voted in favor. In particular, Commissioner Peirce expressed concern that the Commission is acting "fast and loose" with the concept of materiality in proposing such sweeping changes related to climate disclosures and that the resultant disclosure requirements would not achieve stated goals of requiring comparable, constituent, and reliable information across registrants. Commissioner Lee, on the other hand, who has been at the forefront advocating for enhanced disclosure requirements described this as a watershed moment and highlighted aspects of the proposal that will ensure consistency and reliability across registrants.

Stakeholders have 30 days after publication in the Federal Register or May 20 (which is 60 days after issuance), whichever is later to comment on the proposed rule. Given the flood of input on acting chair Lee's initial request for comment on these issues, the SEC is sure to have myriad perspectives to sift through in promulgating the final rule, which likely will not come out for many months.

Arnold & Porter's Environmental, Social and Governance working group has been actively monitoring and advising in this area. Stay tuned for our forthcoming in-depth advisory on the proposed rule. Please reach out to any of the authors or your regular Arnold & Porter contact to discuss the proposed rule and how to stay ahead of this fast-moving landscape.

Table 1: Phase-in Schedule (Source: Fact Sheet)

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.