BACKGROUND

Sustainability is an important focus area for Danish enterprises. Focus on sustainability matters is not only an expectation from stakeholders, but is also becoming an increasingly regulated area where enterprises become subject to enhanced requirements, including with respect to reporting and governance.

In this presentation we provide an introduction to key trends related to sustainability governance and reporting by offering examples and statistics from Danish OMXC251 companies (the "Companies") for the financial year 2021.

The presentation is based on publicly available information found in the Companies' sustainability reports for the financial year 2021.2 The information provided by the Companies has not been independently verified, and direct comparison among the Companies is, at times, not possible owing to different terminology, focus and structure.

This presentation uses the term "sustainability" to cover a broad range of legal and commercial considerations that include other terms such as "CSR" (Corporate Social Responsibility) and "ESG" (Environmental, Social and Governance).

In this presentation, BoD= Board of Directors, ExMa= Executive Management and percentages are to one decimal place.

This presentation is not exhaustive and is for illustrative purposes only. It is not intended to provide legal advice.

INTRODUCTION

Financial Statements Act: Statutory reporting

Sections 99a(1) and (2) of the Financial Statements Act3 state that large companies must supplement the management commentary with a non-financial CSR report.4

The report must include information on environmental matters, social and staff matters, and matters relating to human rights, anti-corruption and bribery, including policies and processes related thereto.

If a company does not have CSR policies, the management commentary should state why.

Recommendations on Corporate Governance

The Corporate Governance Recommendations5 include several recommendations relevant in relation to sustainability. For instance, the Recommendations (1.4.1) state that the board of directors is recommended to approve a policy for the company's CSR, including social responsibility and sustainability, and recommend that the policy be accessible in the management commentary and/or on the company's website.

The board of directors should continuously ensure that the company complies with the CSR policy, and the company should consider to report CSR development and any new measures on its website on an annual basis.

Proxy advisors

Proxy advisory firms, especially Institutional Shareholder Services Inc. ("ISS") and Glass, Lewis & Co. ("Glass Lewis"), play an increasingly influential role in Danish corporate governance by providing shareholders with recommendations on how to vote at general meetings of listed companies (thereby influencing voting outcomes).

Both ISS and Glass Lewis have made separate voting recommendations on sustainability, respectively International Sustainability Proxy Voting Guidelines and Policy Guidelines on ESG initiatives.

EU Taxonomy Regulation and Disclosure Regulation

The EU Taxonomy establishes a green classification system for determining the degree to which an economic activity is environmentally sustainable. It is a transparency tool introducing mandatory disclosure obligations on certain companies and investors, requiring them to disclose their share of Taxonomy-aligned activities.

The Sustainable Finance Disclosure Regulation (SFDR), effective from 10 March 2021, imposes new transparency and disclosure requirements on financial market participants at both the product and entity level, distinguishing in general between (i) financial products with sustainable investment as their specific objective and (ii) financial products that promote environmental and/or social characteristics.

Companies in the benchmark analysis

| C25 companies 20216 | C25 companies 20206 | ||

| A.P. Møller-Mærsk A/S Ambu A/S Bavarian Nordic Carlsberg A/S Chr. Hansen Holding A/S Coloplast A/S Danske Bank A/S Demant A/S DSV A/S FLSmidth & Co. A/S Genmab A/S GN Store Nord A/S |

H. Lundbeck A/S7 Jyske Bank A/S(New) ISS A/S Netcompany Group Novo Nordisk A/S Novozymes A/S Pandora A/S ROCKWOOL International A/S Royal Unibrew A/S Tryg A/S VestasWind Systems A/S Ørsted A/S |

A.P. Møller -Mærsk A/S Ambu A/S Bavarian Nordic Carlsberg A/S Chr. Hansen Holding A/S Coloplast A/S Danske Bank A/S Demant A/S DSV A/S FLSmidth & Co. A/S Genmab A/S GN Store Nord A/S |

H. Lundbeck A/S ISS A/S Netcompany Group A/S Novo Nordisk A/S Novozymes A/S Pandora A/S ROCKWOOL International A/S Royal Unibrew A/S SimCorp A/S Tryg A/S Vestas Wind Systems A/S Ørsted A/S |

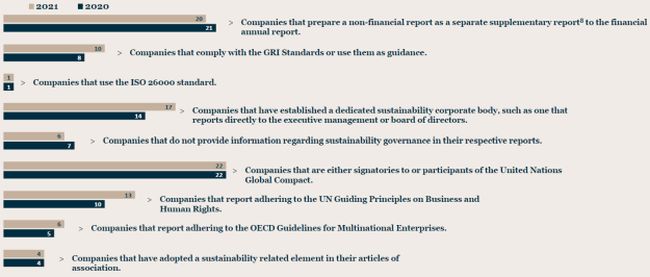

Development in sustainability reporting for OMXC25 Companies

Click here to continue reading . . .

Footnotes

1) OMXC25 currently comprises 24 companies as A.P. Møller-Mærskis counted twice owing to share class sizes.

2) 2021/2022 for companies with a non-calendar financial year.

3) Regulation based on Non-Financial Reporting Directive, which is expected to be replaced by the new Corporate Sustainability Reporting Directive.

4) Financial institutions are covered by Executive Order no. 281 of 5 September 2014. Section 135 imposes disclosure obligations on corporate sustainability.

5) The Recommendations on Corporate Governance (the "Recommendations") are prepared by the Danish Committee on Corporate Governance. In accordance with section 107b of the Financial Statements Act, listed companies must include a statement on corporate governance in which they are required to consider the Recommendations and either comply with them or provide explanations of alternative practices.

6) A.P. Møller -Mærskhas two listed shares, but only one is included.

7) In 2022, Nordea Bank replaced H. Lundbeckin the OMX Copenhagen 25 Index. As this benckmarkis based on information from the financial year 2021, the report will not reflect the change made to the index in 2022.

8) The Companies refer to their non-financial report as "Sustainability report", "CSR report" or "ESG report", and these are allincluded in the diagram.

Originally published 24 October 2022

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.