ASIC has released its enforcement priorities for 2024 outlining the key areas where its resources and expertise will be directed in order to protect market integrity, consumers, and investors.

New Priorities for 2024

New priorities that relate to small business, compliance with the reportable situation regime, gatekeepers that facilitate misconduct, used car financing and market operators were added to the 2024 priorities list.

ASIC's 2024 priorities include:

- Member services failures in the superannuation sector;

- Misconduct resulting in the systematic erosion of superannuation balances;

- Insurance claims handling (with the focus on delays in claims handling, poor communication and record keeping, and inappropriate use of exclusions);

- Compliance with the reportable situations regime;

- Conduct impacting small businesses including small business creditors;

- Enforcement action targeting gatekeepers facilitating misconduct;

- Misconduct relating to used car financing to vulnerable consumers including brokers, car dealers and finance companies;

- Compliance with financial hardship obligations; and

- Technology and operational resilience for market operators and market participants.

Continuing Priorities from 2023

In addition, ASIC will continue to keep its focus on the following 2023 priorities:

- Enforcement action targeting poor distribution of financial products;

- Misleading conduct in relation to sustainable finance including greenwashing; and

- High-cost credit and predatory lending practices to consumers and small business.

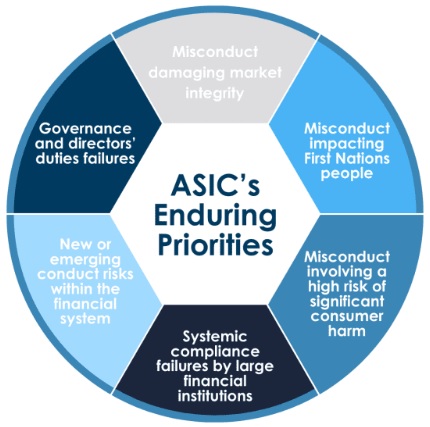

Enduring Priorities

Notably, ASIC has elevated the importance of governance and directors' duties failures by moving it from the 2023 list of priorities to a list of enduring priorities.

The 2023 list of enduring priorities will remain the same for 2024:

- Misconduct damaging market integrity (including insider trading, continuous disclosure breaches and market manipulation);

- Misconduct impacting First Nations people;

Misconduct involving a high risk of significant consumer harm (particularly conduct targeting financially vulnerable consumers);

Systemic compliance failures by large financial institutions (resulting in widespread consumer harm); and

New or emerging conduct risks within the financial system.

What does this mean for licensees?

Licensees should continue to expect that ASIC will actively enforce the law, with a particular focus on its enduring and 2024 list of priorities. Licensees should review ASIC's enforcement priorities and consider how compliance processes and procedures can be further enhanced to ensure robust and reliable compliance outcomes.

Further Reading