On November 10, 2022, the Biden Administration proposed a major new rule aimed at addressing the Federal government's exposure to climate-related financial risks in its supply chains. The Federal Acquisition Regulatory Council (FAR Council) has issued a proposed rulemaking to amend the Federal Acquisition Regulation (FAR). Interested parties have until January 13, 2023 to submit comments.

The proposed Federal Supplier Climate Risks and Resilience Rule would require "major" and "significant" Federal contractors to publicly disclose their greenhouse gas (GHG) emissions and climate-related financial risks and set science-based emissions reduction targets.

The majority of companies in these categories would need to take steps to come into compliance with the proposed rule: Only 31 percent of "major" contractors and 10 percent of "significant" contractors already report disclosing their GHG emissions through the System for Award Management (SAM).

The proposed rule is intended to impact companies beyond those specifically subject to the reporting requirements. The U.S. government is the world's single largest purchaser of goods and services. Incentivizing the greening of Federal supply chains through expanded climate disclosure requirements for Federal contractors will have ripple effects across the domestic economy and internationally. All companies should therefore pay close attention to the progress of this rulemaking and the standards it proposes companies use for purposes of their disclosures.

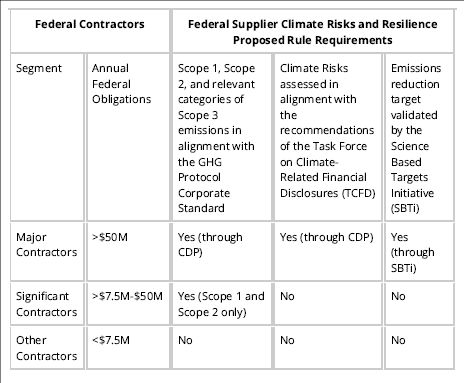

The specific requirements for covered contractors are as follows:

- "Major" Federal contractors receiving more than $50 million in annual contracts would be required to publicly disclose Scope 1, Scope 2, and relevant categories of Scope 3 emissions,1 disclose climate-related financial risks, and set "science-based emissions reduction targets" (defined as targets in line with the goals of the Paris Agreement)

- "Significant" Federal contractors with more than $7.5 million in annual contracts but less than $50 million would be required to report Scope 1 and Scope 2 emissions.

Major contractors that are small businesses with over $50 million in annual contracts would only be required to report Scope 1 and Scope 2 emissions in SAM, and Federal contractors with less than $7.5 million in annual contracts would be exempt. Other limited exceptions (e.g., state or local government, non-profit research entity) have also been proposed.

Available at: https://www.sustainability.gov/federalsustainabilityplan/fed-supplier-rule.html

The proposed rule relies on four existing and well established disclosure standards, including the GHG Protocol Corporate Accounting and Reporting Standards and Guidance, the 2017 Task Force on Climate-Related Financial Disclosures (TCFD) Recommendations, the Carbon Disclosure Project (CDP) Climate Change Questionnaire, and the Science Based Targets Initiative (SBTi) criteria. The FAR Council has invited comments on "the use of these standards in this proposed rule, including potential alternatives to be considered in the formation of the final rule."

The proposed rule would create a new FAR subpart 23.XX, entitled "Public Disclosure of Climate Information," to expand climate-related representations already provided for at FAR 52.223-22 and FAR 52.212-3.

In addition, the proposed rule establishes a new standard of responsibility by providing that a contracting officer is required to treat a significant or major contractor as nonresponsible unless it has inventoried its annual GHG emissions and disclosed its total annual emissions in SAM. Under FAR 23.XX03(b), a major contractor shall also be treated as nonresponsible unless it has made available on a publicly accessible website an annual climate disclosure that was completed using the CDP Climate Change Questionnaire in the current or previous fiscal year and set targets to reduce its emissions. By tying compliance with these climate-related disclosure requirements to responsibility standards for prospective contractors, the FAR Council is incentivizing adherence to the proposed rule's reporting requirements as the FAR requires an affirmative determination of responsibility for federal contract awards.

Starting one year after publication of a final rule, significant and major contractors must have completed a GHG inventory and must have disclosed total annual Scope 1 and Scope 2 emissions from their most recent inventory in SAM. Starting two years after publication of a final rule, major contractors will be required to complete a GHG inventory that covers relevant Scope 3 emissions; conduct a climate risk assessment and identify risks; complete the CDP Climate Change Questionnaire; and commit to, develop, and obtain SBTi validation of a science-based target. There are also limited exemptions and waivers of certain procedures "for national security purposes, or for emergencies, national security, or other mission essential purposes," and for the possibility of granting an entity additional time to come into compliance (1 year).

Even with these delayed start dates, companies unfamiliar with the proposed standards would benefit from preparing to comply given the highly technical nature of the disclosure requirements and the GHG inventory process in particular. As the proposed rule notes, companies completing a GHG inventory for the first time will need to review accounting standards and methods, determine organizational and operational boundaries, collect data from across the business (including but not limited to fuel purchases, such as gasoline and heating oil, and electricity bills) and utilize a GHG calculator to determine the associated GHG emissions emitted across Scope 1, Scope 2, and (if applicable) relevant Scope 3 emissions expressed in MT CO2e. Companies should also consider how the proposed rule may interact with other mandatory and voluntary climate-related disclosure obligations and the implications of potential interactions for their internal compliance processes.

The Securities and Exchange Commission (SEC) recently proposed a regulation that if adopted would require similar annual disclosures of climate-related financial risks for SEC registrants, including publicly listed/traded companies, many of whom are also Federal contractors. The SEC's proposed rule, which was issued in March 2022, would require registrants to disclose climate-related financial risks and related metrics, including GHG emissions metrics, in their registration statements and annual reports. A link to Steptoe's advisory discussing the SEC rule, entitled "[t]he Enhancement and Standardization of Climate-Related Disclosures for Investors" is available here. Like the proposed FAR rule, the SEC's proposed rule also leverages existing standards, such as the GHG Protocol Corporate Accounting and Reporting Standard and the recommendations of the TCFD. However, the SEC's proposed rule does not include a requirement for SEC registrants to set science-based targets; it only proposes that SEC registrants, including publicly listed/traded companies, disclose targets if they have adopted them. By contrast, the proposed FAR rule specifically requires that major and significant federal contractors provide an annual climate disclosure that was completed using the CDP Climate Change Questionnaire and that major contractors set science-based targets to reduce their GHG emissions.

Footnote

1. Scope 1 emissions include GHG emissions from sources that are owned or controlled by the subject entity; Scope 2 emissions include GHG emissions associated with the generation of electricity, heating and cooling, or steam, when these are purchased or acquired for the subject entity's own consumption but occur at sources owned or controlled by another entity; and Scope 3 emissions are a consequence of the operations of the subject entity but occur at sources other than those owned or controlled by the entity.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

We operate a free-to-view policy, asking only that you register in order to read all of our content. Please login or register to view the rest of this article.