Expectations for a second-half 2023 rebound for volume and pricing in the logistics and shipping industry have been thwarted by slower-than-anticipated demand and global trade developments. Meaningful recovery in freight conditions won't likely manifest until at least the first half of 2024.

Industry players and investors cannot sit still in the meantime. Ocean carriers have the cash to deploy on strategic initiatives, including mergers and acquisitions, restructuring, or operational improvements. Shippers can leverage favorable pricing to reevaluate supply chain needs and prepare for further disruption.

For in-depth coverage of market conditions, listen to Marc Iampieri's views on expectations for the remainder of 2023 in this recent edition of GrowthX's Logistics, Supply Chain & Transportation podcast.

What's driving market conditions?

Several important factors are fueling the near-term downturn in volume and pricing.

Many retailers – from Walmart to Home Depot – see continued pressure on consumer spending as the marketplace focuses on basic necessities over discretionary purchases and shifts more dollars to experiences and services. Several big box chains have lowered full-year outlooks as a result.

U.S. manufacturing activity has been contracting for several months, dealing another blow to optimism. The weakness has been widespread, with factory slowdowns also recently reported for China and the Eurozone.

Inventory planning, meanwhile, is severely disjointed – a condition that continues to challenge companies several years after the pandemic outbreak created unprecedented chaos in global supply chains. With demand forecasting derailed, inventories are stuck in a state of misalignment.

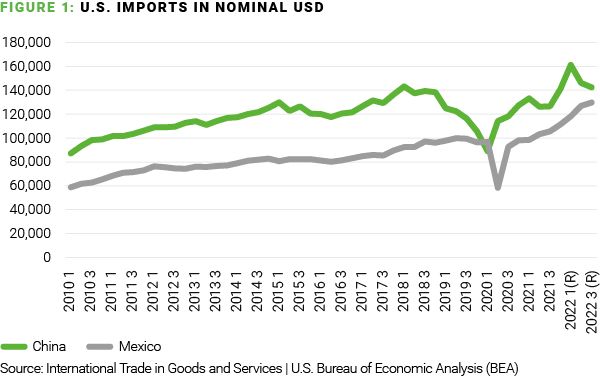

Global trade trends are further complicating the picture. In a push to deleverage from China, reshoring and nearshoring are gaining momentum. More companies are sourcing from Vietnam, for instance, while nearshoring is showing a sharp uptick (figure 1).

This rebalancing affects demand flows for logistics around the world. Rates in China, for instance, are lower. At the same time, rates are increasing in other regions, such as the South America-to-U.S. lane.

A look at individual modes

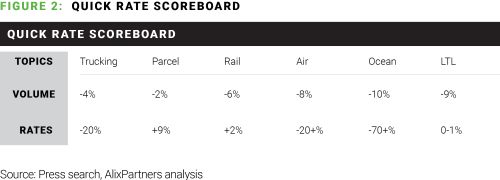

Ocean

Ocean volumes are down 10% overall, and port terminals are underutilized. Net income for ocean carriers in 2023 is roughly 70% lower than the same period in 2022, but still above historical pre-pandemic averages. While carriers will likely be profitable this year, proceeds will be tamer than they were in recent years.

There are several challenges facing carriers. Green fuel regulations, for instance, impact fuel availability and cost, and the EU is proposing new enhanced regulations. Drought conditions in Panama are raising the possibility of reduced payloads or diversions, which add time and cost to transit.

There has also been an alliance shakeup – with the top carriers now large enough to operate outside of an alliance, the 2M partnership is dissolved. Any further changes could impact pricing and capacity as it unlocks more competition between carriers.

Global container production hit a 14-year low. At the same time, operators are forced to balance automation and labor dynamics. The now-resolved recent port strike on West Coast provided a reminder of the vulnerability the industry faces.

Warehousing

Vacancy rates have recently trended up, but not quite back to pre-COVID levels. Inventory-to-sales ratios have been steadily increasing, keeping demand for warehouse space high. Industries, in fact, are increasing inventory due to buffer stock, supply chain challenges, and other factors.

Warehousing remains a brighter spot in the logistics market as rates stay strong amid a slower inventory build. Specifically, there is demand for cold storage, and customers are returning more goods leading to a requirement for more storage space.

Trucking

Expectations call for a bottoming out of trucking rates by the end of 2023, followed by a rebound in 2024. In the immediate term, nearshoring is impacting rates in Mexico and triggering the expansion of logistics firms south of the U.S. border.

Among the trends to watch are fuel prices; diesel and gasoline prices are down 30% year-over-year. Additionally, consolidation is beginning to ramp up as more companies are closing operations.

The sector is also affected by home delivery operations that are underperforming for many key retailers, even as one-day delivery gains momentum. A growing number of shoppers also are increasing the amount of goods they return.

Rail

Rail service has improved slightly in the first half of 2023, but Western carriers need to continue their drive to be more customer-centric. The investments railroads and customers are making across the business can help drive growth in future years.

Volume continues to be challenging, with intermodal down nearly 11% year to date, driven largely by West Coast port impacts. Railroads have also reached labor agreements with many unions so far in 2023, securing sick leave and other benefits for crews.

There will likely be an increased level of focus on safety and potential regulation over the remainder of 2023 amid continued fallout from the devesting derailment earlier this year in East Palestine, Ohio.

Tight labor conditions are still a thorn for rail operators. Additionally, low import volumes are raising pressure on intermodal transport. Demurrage fees continue to create issues.

Air

The overall air market is soft, and the condition is exacerbated by a glut of air cargo capacity that is further affecting spot rates this summer. FedEx aircraft utilization dropped 10% in April, suggesting more short-term pain in the market. In addition, new entrants are continuing to enter the market, further impacting rates.

The time to act is now

Cash generated over from the past two years — records for ocean carriers —should be used to fund M&A, restructuring, and operational upgrades.

New trade lanes are opening additional opportunities to develop strong long-term relationships, with nearshoring being an example. Investments in automation and digitalization can increase the strategic advantages of firms for future economic expansion.

Additional strategic acquisitions can be made during this rough patch to set companies up for the future. Distressed asset/debt sales will present opportunities for consolidation, as smaller firms or highly leveraged firms struggle in the low-price environment.

For shippers, meanwhile, this relative calm in the market gives companies time to evaluate production and other internal processes to overhaul operations.

To be sure, potential OPEC cuts could pressure fuel costs, and Federal Reserve policy could negatively affect inflation, unemployment, and the overall economy. Still, market conditions and the economy are resilient right now, leading to a second half of the year that will be important regarding inventory buildup from the consumer and industrial sectors.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.