As global markets continue to adapt to a new normal, a clear understanding of the structural nuances, risk considerations, and strategic objectives inherent in varying transaction structures enables investors to remain agile and secure advantageous transactions in the evolving market landscape. This article explores several of the differentiating factors and deal-term considerations of M&A buyouts and significant minority growth equity investments, both essential components of a deal maker's toolkit.

Understanding the Deal Structures

M&A Buyouts: Majority Ownership and Full Control

M&A buyouts contemplate the acquisition of a controlling interest in a target company, leading to a complete or majority change in ownership. Through the acquisition, investors obtain control of the target, which ensures decision-making power.

Growth Equity Transactions: Partnership Without Full Control

In contrast, minority growth equity deals are characterized by an investor acquiring a non-controlling stake in the company. Minority growth equity deals typically fall into two categories: smaller minority investments, involving up to 10%-15% ownership through preferred equity rounds; or significant minority growth equity investments, through which an investor acquires up to 50% minority stake in the target company. This article will focus on the latter type of growth equity investments, in which investors bet on the target's potential for significant growth and a lower risk of capital loss as compared to early-stage ventures. Significant minority growth equity deals contemplate existing shareholders retaining a majority share, which leads to a more complex capitalization table and a nuanced dynamic in company governance and future fundraising efforts.

Key Differentiating Factors

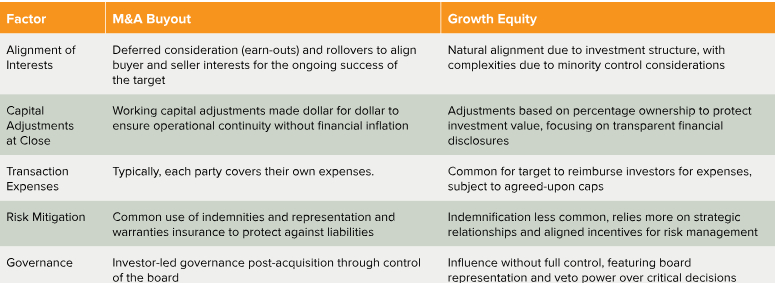

Alignment of Interests

In M&A buyouts, deferred consideration (i.e., an earnout) is a tool that is often used to help bridge valuation gaps, with part of the purchase price deferred to a future date and often tied to performance milestones. This construct aligns the interests of buyers and sellers by giving the sellers an interest in the ongoing success of the target company while also mitigating the buyer's risk related to the business's future performance. Similarly, rollover equity serves as a mechanism for sellers to reinvest a portion of their proceeds back into the target, signaling confidence in its prospects and again aligning sellers' interests with those of the buyer. This type of reinvestment allows sellers to share in the future financial performance when the target is later sold or goes public and creates a partnership-driven approach among the parties.

In growth equity transactions, the acquisition by an investor of a minority stake of a target naturally aligns incentives among the parties, akin to rollover and deferred consideration constructs. With equity holders retaining a majority of the target, growth equity structures organically fulfill the purpose that rollover and deferred consideration structures serve in M&A buyout transactions. However, given investors do not obtain control in growth equity transactions, corporate governance structures are heavily negotiated and specifically tailored to provide investors some degree of control over management decisions affecting the target. In contrast, M&A buyouts generally result in investors obtaining control over decision-making, so sellers receiving rollover equity or deferred consideration may attempt to negotiate certain rights to ensure the investor's business practices do not cause the target to cease to perform in a material manner, thereby diminishing the potential value of any deferred consideration.

Capital Adjustments at Close

Working capital adjustments are important in both M&A buyouts and growth equity deals as they incentivize the target's management team to operate the business in the ordinary course, preventing the artificial inflation of financial metrics (e.g., receivables, inventory, etc.) before the closing of a transaction. In M&A buyouts, these adjustments safeguard the buyer from inheriting a business that requires additional funding to operate immediately following the consummation of the transaction, while in growth equity deals, they similarly protect the investment value by ensuring the company has sufficient operating capital and current assets.

The nuances of working-capital adjustments differ between M&A buyouts and growth equity deals. In M&A buyouts, the purchase price is often adjusted dollar for dollar based on changes in working capital as measured against a target amount. Because investors gain complete ownership of the target, they also receive full access to financial and other data to validate working-capital figures following closing, thereby resulting in more accurate post-closing working capital calculations. Conversely, in growth equity deals, any purchase price adjustment investors receive most often proportionally corresponds to the percentage of the business acquired (reflecting the fact that investors do not own the entire business). Additionally, investors in growth equity deals may face challenges in accessing the comprehensive financials and other information necessary to validate working-capital figures, putting them at a relative disadvantage. One way minority investors overcome this information asymmetry is to require a target to deliver its good-faith financial statements to the investors within a certain amount of time post-closing to allow for investors to determine if any working capital adjustment is necessary.

Transaction Expenses

Reimbursement of transaction expenses also vary depending on deal structure. In M&A buyouts, each party customarily covers its own transaction expenses, with the target's and/or seller's transaction expenses being paid from the deal consideration proceeds at closing. In growth equity deals, the target may reimburse the investors for a portion of their transaction expenses.

Risk Mitigation – Indemnities

Indemnities in M&A buyouts typically provide broad protection against certain liabilities that the parties agree the sellers should bear (e.g., indemnities for breaches of seller's representations and warranties, breaches of seller's post-closing covenants, and liabilities with respect to pre-closing taxes). Other specific indemnities in M&A buyouts may be negotiated and are also informed by the existence of buyer representation and warranty insurance (RWI) policies and the coverage obtained thereunder. In contrast, growth equity deals may or may not include indemnity terms, and parties may choose to negotiate indemnification constructs in circumstances in which breach-of-contract claims with respect to representations and warranties and covenants alone would not provide sufficient recourse. Additionally, in both M&A buyouts and in the growth equity context, investor indemnity protections are often subject to certain limitations on recovery such as traditional caps and baskets.

Indemnities in the growth equity context also present unique challenges that may not otherwise be present in M&A buyouts. For example, in M&A buyouts, indemnities in favor of the buyer must be paid by the seller, and the amount the buyer can recover is subject only to any limitations specifically contained in the purchase agreement (e.g., caps, baskets, source of funds, RWI policy, etc.). In growth equity deals, however, parties must consider and provide for the appropriate mechanics of indemnity claims brought by investors (e.g., [i] whether the target or the equity holder will provide the indemnity, [ii] whether the investors or the target will receive the benefit of the indemnity, [iii] whether investor losses should be calculated considering their pro-rata ownership of the target, and [iv] whether indemnity recovery should be in the form of cash or an adjustment to investor ownership).

Risk Mitigation – RWI

In the RWI market, coverage for growth equity deals typically reflects the investor's pro-rata ownership of the target. Fundamentally, growth equity style coverage is intended to make the minority investor whole for its losses resulting from a breach of a representation or warranty, which would be a prorated amount in the case of losses directly incurred by the target because the investor does not fully own the target, but a non-prorated amount in the case of any losses directly incurred by the investor. Another difference for such growth equity–style coverage is that the retention under the policy would be based on the investor's pro-rata portion of the enterprise value, rather than the total enterprise value. If the investment amount is close to 50%, some insurers may be willing to provide M&A buyout-style coverage without the fixed proration approach. In this case, the RWI policy would be structured like an M&A buyout deal with a significant rollover, such that the policy terms allow the insurer to prorate losses if a breach was known to the party making the representation and warranty. In such M&A buyout-style coverage, the retention would be based on the full enterprise value.

Governance

The relationship between investors, founders, and existing shareholders is also a key differentiator. In M&A buyouts, investors may choose to pursue changes in operational management or strategic direction, while growth equity deals typically see investors working alongside existing management. This partnership approach in growth equity fosters collaboration, with investors providing capital, strategic guidance, and networking opportunities to fuel the company's growth and innovation.

In M&A buyouts, the go-forward control structure is most often straightforward: the investor gains control over the target by way of control over the board of directors (or a similar governance body). Alternatively, growth equity investments require a more nuanced and negotiated approach with respect to governance, offering the investor influence without outright control. Such terms include board representation for the investor, board observer rights, veto power over key decisions, and preferential exit strategies and transfer terms.

To manage these protections, shareholder and similar agreements in growth equity investments are of vital importance and are highly negotiated instruments. In addition to negotiated terms with respect to the sale and transfer of equity (e.g., drag-along rights, rights of first offer, redemption rights, tag-along rights, etc.), such agreements in growth equity transactions also often address governance terms with respect to the operations of the target (e.g., approval for expenditures over certain thresholds, approval for taking on indebtedness, approval for hiring or firing of key management, etc.). Conversely, in M&A buyouts, shareholder agreements generally look to provide the rollover holders with limited minority protections (i.e., against affiliate transactions).

Conclusion

M&A buyouts and significant minority growth equity deals, each with their unique strategies and objectives, play crucial roles in the landscape of corporate transactions. Understanding their nuances, from financial adjustments and risk management to investor protections and stakeholder relationships, is essential for making informed investment decisions and achieving long-term success.

The choice between these two transaction types should be guided by the investor's strategic goals, risk tolerance and the operational stage of the target company. M&A buyouts offer a pathway to complete control, which facilitates significant strategic shifts and integration benefits. In contrast, growth equity transactions foster partnership and innovation, offering a viable alternative in a market in which current owners are reluctant (or unable) to fully exit their investments.

As the global market continues to evolve, the ability to adeptly navigate between these investment strategies becomes increasingly important. Investors must stay informed and flexible, adapting their approaches to align with shifting market conditions and stakeholder expectations. This agility will be key to capitalizing on opportunities and achieving sustained success.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.