While much of the development of ESG can be attributed to demands by investors and consumers, regulations are emerging to put requirements around companies' stated ESG-reported outcomes. In the wake of Russia's invasion of Ukraine, leaders in the European Union ("EU") met in March to discuss strengthening defense capabilities, reducing energy dependency, and building a growth and economic investment model for 2030. The Versailles Declaration, adopted by EU leaders in March 2022, addresses Russia's aggression toward the Ukraine and calls for building on Europe's strengths to make its economic base more resilient, competitive, equitable, and fit for the green and digital transition.

Enabling the transformation to a sustainable economy is a key political priority of the EU Commission's 2021 Corporate Sustainability Reporting Directive ("CSRD"), which amends existing reporting requirements under the Non-Financial Reporting Directive ("NFRD"), as well as the Corporate Sustainability Due Diligence Proposal Directive ("DD Directive"), adopted in February 2022. The CRSD enacts more detailed sustainability reporting requirements and stringent audit requirements. As a further reporting step, the DD Directive includes a requirement for EU states to develop their own mandatory laws to form a clear framework to support companies to create a fair and sustainable economy and society. Particularly, the DD Directive charges companies beyond a certain size to develop and maintain policies aimed at establishing, improving, and demonstrating their ESG performance. While it is subject to a comment period of 1-2 years followed by another approximately two-year implementation period, companies can take actions now to convert the associated risk factors into opportunities. For example, as companies emerge from the disruption of COVID, they can address the inefficiencies and interruptions in their supply chains to assess their diligence procedures directly related to human rights and the environmental impact associated with their suppliers. Once fully implemented, the DD Directive will likely require governments to penalize and fine companies for noncompliance with their duty to identify, mitigate, and account for adverse human rights and environmental impact – internally, and as associated with their suppliers.

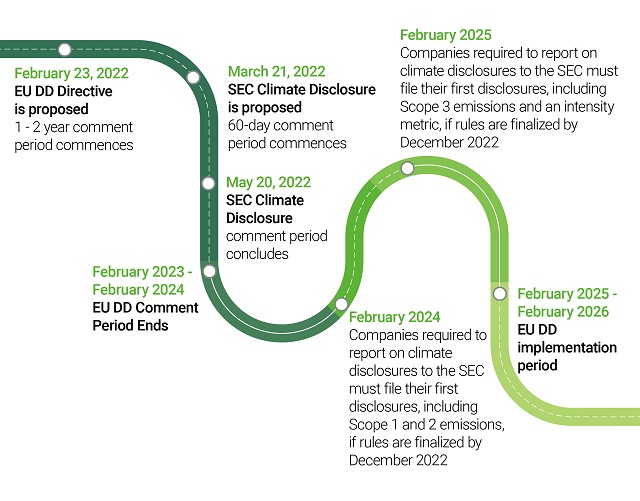

Beyond the EU, the DD Directive will apply to non-EU based companies if they have operations within the EU that (i) either generate a net turnover of more than Euro 150 million in the EU or (ii) with a turnover between Euro 40 million and Euro 150 million in the EU but active in the textile, agriculture or extraction of mineral resources sectors. Issuers within the U.S. can also expect likely forthcoming requirements on climate change disclosures from the Securities and Exchange Commission's proposal currently in the 60-day comment period.1

Below is a high-level perspective of the timeline for adoption and roll-out of the DD Directive along with some other recent global regulations, including the U.S. Securities and Exchange Commission's recent proposal on climate disclosures.

How can companies address and make impactful changes to build resiliency through ESG implementation?

Historically investors, consumers, and other market participants have levied demands on how a company considers and integrates climate change and ESG. As such, share price and/or future business opportunities may be directly or indirectly affected by a company's performance in this area.

Beyond market pressures, increasing EU regulation has mandated expedited ESG integration and more transparent reporting, making ESG simple table stakes with definitive winners and losers. Below are five proactive actions that can help companies to ensure they're on the right side of this equation.

- Assess and update risk management process and related tools to include requirements around climate change and emerging ESG regulations and investor and consumer expectations. Conduct a critical review of business units and operations to understand resilience, opportunities, and risks posed by ESG and climate change.

- Re-evaluate corporate strategy relative to ESG issues with a lens for innovation and opportunity. This includes setting goals, developing roadmaps to achieve them, and factoring in short and long-term strategies.

- Strengthen governance structure and resiliency goals, establishing a framework for policies, procedures, and controls aligned with ESG goals and integrated into company leadership performance expectations to promote accountability and adaptability. Incorporate specific goals and measures relative to how resiliency will be enhanced by ESG development. To effectively do this, appoint an ESG champion who is also independently accountable to the Board.

- Set ESG goals and develop related targets and KPIs to evidence and report on progress periodically both internally and externally. Consider financial and non-financial reporting requirements in all jurisdictions where regulations apply.

- Evaluate marketing messaging, ensuring transparent and accurate communication and aligning with financial and non-financial reporting to avoid greenwashing.

1 SEC.gov | SEC Response to Climate and ESG Risks and Opportunities.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.