Background

Private equity (PE) funds with at least two German tax resident investors are required to file an annual partnership tax return in Germany, even if they do not have taxable presence in the Germany.

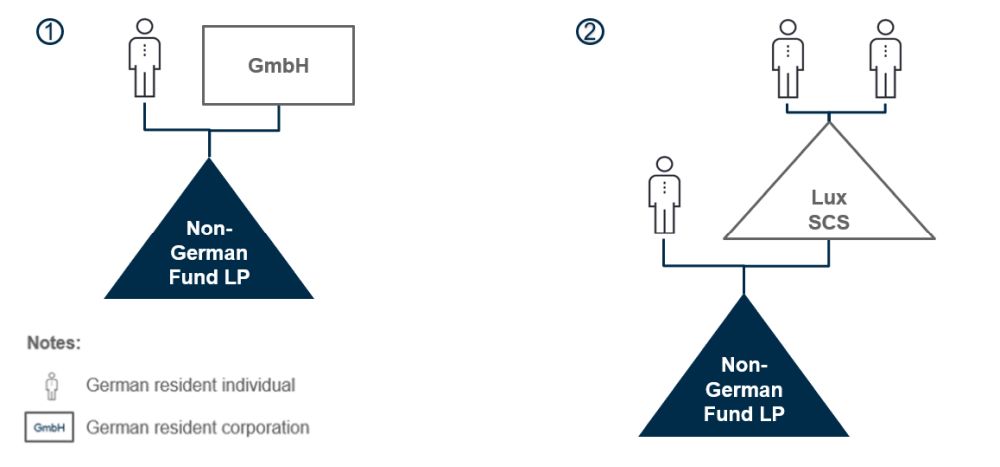

From basically 2023 onwards PE funds (not the German investors) are liable for filing a partnership tax return – comparable to a K-1 tax form in the U.S. – in the following scenarios:

- Two German residents (individual or corporate) directly invested in the fund.

- German tax residents invested in the fund via transparent non-German entities (e.g. Lux SCS).

Failing to file the required annual partnership tax return in Germany may result e.g. in the fund's late filing penalties or in the tax authorities' tax estimate at the German investor level.

While funds with only one German investor are not required to file a partnership tax return, they might still need to assist German investors with their tax reporting to support side-letter agreements, for example by providing the German investor with a pro forma tax reporting in order for the investor to include the fund income in the his individual (corporate) income tax return.

Key considerations for PE funds

Preparing the partnership tax return requires an in-depth analysis of the fund structure in order to:

- Qualify the fund as a (deemed) business partnership or asset management partnership;

- Qualify the entities within the structure as opaque (corporation) or transparent (partnership);

- Qualify and quantify the German investor's income according to German tax law.

In addition to analyzing investment structures carefully, funds must verify:

- Whether a distribution within the fund structure qualifies as a tax neutral Return of Capital (RoC) for German tax purposes which requires an application with the German tax authorities by the distributing entity. In the absence of such application the RoC is treated as a (fully) taxable dividend at the level of the German investors; and

- Whether corporate entities within the fund structure have net passive income (e.g. interest income): German investors have to file a a tax return in case of CFC / PFIC income (in addition to the partnership tax return).

Originally published by 29 May, 2024

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.