Dewan")

‎")

India is one of the world's fastest growing economies, and with its consistent GDP growth, favourable demographics supporting steady consumer spending and continued focus on infrastructure investment and development, it provides a promising investment opportunity with robust macroeconomic fundamentals. India's GDP growth is projected to hit seven percent in 2026, according to latest estimates from S&P Global. Goldman Sachs recently raised its forecast for India's GDP growth in 2024 to 6.6 percent, from 6.5 percent estimated earlier, on account of higher investment spending. This reflects both global and domestic optimism in the country's economy. In 2023, India's stock exchanges saw more IPO's than any other jurisdiction, where IPO proceeds totalled US$7.89 billion.

The notable surge in foreign direct investment inflows in India in the recent years has been attributed to the government's comprehensive market-oriented policy reforms, proactive investment facilitation, and domestic policy aimed at growing investments in India's infrastructure and renewable energy sectors. Such key initiatives have created a conducive environment for foreign investors, fostering increased confidence and participation in the country's economic landscape.

As a result of these and other factors, this is an exciting time for the private equity industry in India, as large global private equity investors continue to set up India-dedicated funds or rebalance their allocation for Indian investments in their global portfolios. Fundraising from dedicated India funds has quadrupled over the last decade, growing from $1.9 billion in 2012 to $8.0 billion in 2022. The average fund size has also increased from $86 million in 2012 to $160 million in 2022. Currently, it is estimated that there are more than 200 private equity firms investing from dedicated India funds, while foreign investment inflow in India peaked at US$71 billion in 2023. India has also benefited from capital outflows emanating from a number of global private equity firms, sovereign funds and North American public pension funds who have diversified their portfolios from China and redirected capital to India in response to cooling growth, and regulatory and geopolitical tailwinds in China.

Canadian investment in India

In Canada, a number of pension funds and private sector investors have been very active in investing in India and this will likely expand given recent changes which eased foreign investment restrictions in certain sectors, including insurance, space sector, telecom and railway infrastructure. From 2019 to 2023, India replaced China as the second largest recipient of Canadian pension fund inflows into the region. The top three sectors in India to receive investment from Canadian pension funds were real estate, financial services and industrial transportation.

Some notable examples are below:

- The Canada Pension Plan Investment Board ("CPPIB") has invested in India since 2009, and established a presence in Mumbai, India in 2015. As of March 2024, CPPIB has invested around C$28 billion in India, making it one of the largest institutional investors in the country. India's infrastructure investment remains a key market for CPPIB. Recently, in March 2024, CPPIB announced a follow-up investment of C$297 million in the units of National Highways Infra Trust ("NHIT"), an infrastructure investment trust sponsored by the National Highways Authority of India, increasing its total investment in NHIT to C$614 million.

- Brookfield also has a significant presence in India, encompassing a vast real estate portfolio. The company is also expanding its portfolio of solar and wind assets in India, and maintains a diverse private equity portfolio in the region, with investments in healthcare and construction services. Recently, Brookfield Asset Management announced the acquisition of American Tower Corp's (ATC's) Indian operations for US$2.5 billion, positioning it as the largest operator of telecom towers in India. Over the next three to five years, Brookfield plans to invest more than US$10 billion in India to capitalize on the growing real estate industry, aiming to double its real estate assets under management in the country.

- Teachers' Venture Growth Fund (the late stage venture and growth investment arm of the Ontario Teachers' Pension Plan) invested US$80 million into Xpressbees in November 2023, one of the fastest growing end-to-end logistics companies in India. In September 2022, the Mahindra Group (one of the largest Indian conglomerates with over 260,000 employees in over 100 countries) formed a strategic partnership with Ontario Teachers' infrastructure investment trust in India for investing in India's renewable energy sector.

- Fairfax India, an investment holding company, publicly traded on the Toronto Stock Exchange has a robust India focused investment strategy in both public and private equity and debt market in India. Fairfax India's largest investment is the Bangalore International Airport ("BIAL"), the busiest airport in south India and the third largest in the country. As of date, Fairfax India holds a total investment of C$903 million for 64 percent of BIAL. In addition to this, Fairfax India has investments in major players in the Indian financial services sector including IIFL Finance, IIFL Securities and CSB Bank, in the manufacturing sector including Sanmar Chemicals Group and Fairchem organics, as well as in the logistics sector including in the second largest shipping company in India, Seven Islands Shipping.

- Some of the other prominent Canadian investors in India include Sun Life, Polar Asset Management, Caisse de dépôt et placement du Québec and Magna International.

Structuring investments

Offshore investment vehicles and double taxation treaties

India's Double Taxation Avoidance Agreements ("DTAA") regime covers a vast network of DTAA, presently having DTAAs with over 90 countries. So far, foreign investments into India have been primarily structured through the use of an entity established in a jurisdiction with a favourable tax treaty with India. In this respect, a number of jurisdictions have been favourably considered to structure inbound investment, including Singapore, the Netherlands and Mauritius. During 2022-2023, the top FDI source countries for India were Singapore, Mauritius, the US, the UAE, and the Netherlands, contributing 76.5 percent of total FDI equity.

GIFT City

Recently, India set up its first international financial services center ("IFSC"), the Gujarat International Finance Tec-City ("GIFT City"), organized with a view to onshore financial services transactions with an Indian nexus. GIFT City has emerged as a thriving investment haven especially among foreign portfolio investors ("FPIs") who are considering opting for it over traditional investment routes via Mauritius or Singapore. GIFT City offers lucrative tax benefits including a 100 percent tax exemption for ten of the 15-year block period. In addition, there is no goods and services tax (GST) or securities transaction tax (STT) on transactions made on IFSC exchanges. Businesses establishing their operations in the GIFT City benefit from additional incentives such as exemptions from stamp duty and registration fees. GIFT City will also permit Indian issuers to raise foreign currency from international investors. Previously, Indian issuers were limited to raising capital on overseas exchanges through American or Global Depositary receipts.

Foreign businesses are also allowed to raise money through the IFSC without any limitations on the ability to repatriate funds. This enables both domestic and international businesses to access the international markets through GIFT City. Due to these regulatory benefits, funds have started redomiciling from other offshore jurisdictions to GIFT City. In May 2023, Alchemy Investment Management LLP's India Long Term Fund became the first fund to redomicile from Mauritius to GIFT City, with several other funds set to follow. More than 80 fund managers with commitments of $30 billion and investments of over US$2.93 billion have set up funds at GIFT City in the last three years. Although GIFT City offers assured tax benefits backed by regulatory updates, there remains a need for more clarity on certain regulatory requirements as well as tax implications for investors.

Domicile of investing: Mauritius, Singapore and the Netherlands

Currently, most India-focused funds are based out of either Singapore or Mauritius as a limited liability partnership (LLP) or a corporate entity. Mauritius has long been considered as a preferred jurisdiction for investing in India, largely due to the advantageous DTAA with India (the Indo-Mauritius DTAA) that permits foreign investors significant tax benefits in relation to returns on their Indian investments. India and Mauritius have enjoyed close economic, political, and cultural ties for over a century. The two countries have collaborated closely on numerous issues, including trade, investment, education, security, and defense. In the recent years there have been significant changes to the Indo-Mauritius DTAA to monitor treaty abuse for tax evasion purposes. Transactions related to the India-Mauritius DTAA continue to be closely scrutinised by tax authorities in India. The amendment protocol in 2016 provided India a source-based right to tax capital gains (as opposed to the previous residence -based tax regime). Additionally, corporates and FPIs investing in India through Mauritius must now reassess and adapt their strategies to comply with the principal purpose test (PPT). This means that simply having a tax residency certificate issued by Mauritius may no longer be enough to claim tax benefits under the treaty. It would require demonstrating that the primary motivation for establishing an entity in Mauritius is to not solely gain benefits from the India-Mauritius DTAA. The amendments also mandate certain expenditure and residency criteria to prevent treaty shopping and round-tripping of funds. Utilizing an entity established in Mauritius can have its challenges as some investors may not be familiar with Mauritian law. As a result, some structures have been created whereby a parent entity to a Mauritius entity is established (where investors allocate their capital for investment) in an offshore jurisdiction where such investors have more comfort and familiarity with the applicable laws.

Despite these changes, Mauritius continues to be a significant hub for investments into India and continues to be a key element in the strategic investment decisions involving India. The Indo-Mauritius DTAA provides substantial benefits especially in areas like withholding the tax rate for interest income which is significantly lower than those under India's treaties with Singapore and the Netherlands.

Singapore is one of the leading holding company jurisdictions in the Asia-Pacific region, known for its well-established capital markets regime that offers regulatory stability and a favorable investment environment. This makes it advantageous if listing of a fund is contemplated. As of the 2022-23 financial year, Singapore was the largest source of FDI into India. The double taxation avoidance agreement between Singapore and India (India-Singapore DTAA) was co-terminus with the India-Mauritius DTAA, meaning that the benefits under the India-Singapore DTAA were aligned with those of the India-Mauritius DTAA, and exemptions under the India-Singapore DTAA were valid as long as similar benefits existed under the India-Mauritius DTAA. Following the amendment of the India-Mauritius DTAA, India and Singapore signed a protocol in 2016, to amend their DTAA. These amendments introduced source-based taxation of capital gains from the sale of Indian shares held by Singapore residents, replacing the previous residence-based taxation approach.

For inbound investments to India, the Netherlands stands out as an efficient jurisdiction for making portfolio investments. The India-Netherlands tax treaty provides relief from double taxation by exempting certain capital gains from tax in India, both from direct and indirect transfers. Specifically, gains arising to a Dutch resident from the sale of shares of an Indian company to a non-resident buyer are not taxable in India. However, these gains would be taxable for a sale in India by a Dutch resident holding more than ten percent of the Indian company. Despite this cap on eligible holdings, the structure is well-suited for FPIs, who are limited in their holding of an Indian company.

The principal laws governing foreign private equity investments in India are the Foreign Exchange Management Act, 1999 ("FEMA") and rules, regulations, circulars, notifications and press notes issued under FEMA, the Companies Act, 2013; the Income-tax Act, 1961; and the Competition Act, 2002. In the case of listed or to be listed entities in India, the regulations made by the public market's regulator, the Securities Exchange Board of India ("SEBI"), would also be applicable. In addition to the abovementioned general legislations, certain sector-specific laws may also be applicable for regulated sectors such as financial services and infrastructure.

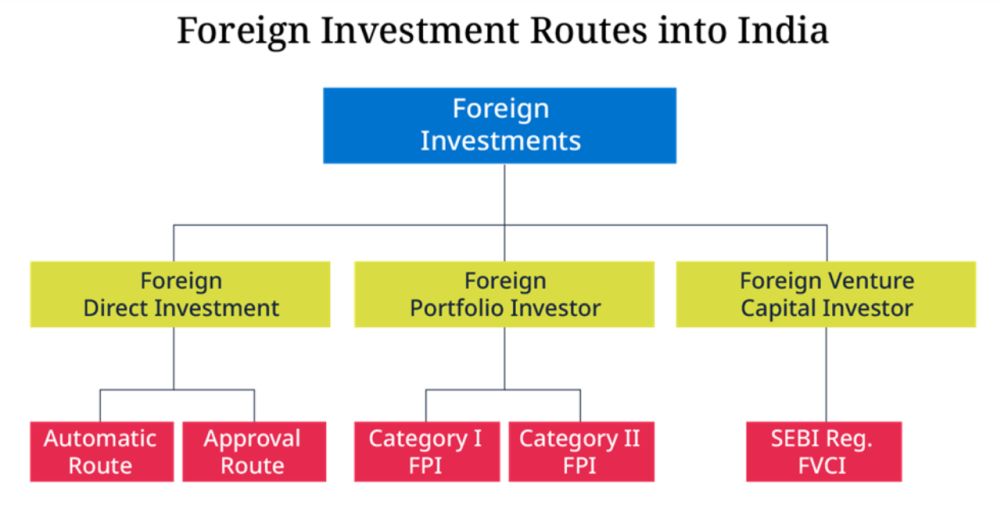

There are broadly three entry routes for private equity investment in India:

Foreign direct investment (FDI)

FDI is the most common mode of foreign investment in India. A private equity investor may invest into India either directly through an offshore entity, or indirectly through an Indian subsidiary. Any investment through this route would be subject to India's foreign investment regulations. These regulations set out the limitations on foreign investment in certain sectors in India. Investment through this route may be done through either the automatic route or the approval route. The applicable route depends on the sector in which the proposed investment is contemplated and the extent of equity to be acquired.

Under the automatic route, a foreign investor would be able to invest in a sector in India without any prior governmental or regulatory approval, such as the hotel and tourism sectors. However, investment done through this route may be subject to certain additional conditions as well as pricing guidelines under the foreign investment regulations, which govern the pricing in transactions between foreign investors and resident Indian investors in any Indian equity securities. For example, while 100 percent FDI is permitted in single brand retails, in cases where foreign investment is proposed to be more than 51 percent, certain domestic sourcing requirements are applicable with at least 30 percent of the value of the goods purchased to be acquired in India, preferably from Indian micro, small and medium enterprises.

FDI is entirely prohibited in certain specified sectors such as 'Lottery Business', 'Trading in Transferable Development Rights' and 'Real Estate Business' (not including development of townships, construction of residential or commercial premises, roads or bridges and Real Estate Investment Trusts (REITs)). There are also sectors with a specific threshold for FDI, sectors that require government approval of the relevant government department or ministry (e.g., for the pharmaceutical sector, the Department of Pharmaceuticals and for the financial sector, the Reserve Bank of India) and, in certain cases, the Indian central government and sectors which are partially under the automatic route and partially under the government approval route. For example, in private sector banks in India, up to 74 percent foreign investment is permitted, in which up to 49 percent is under the automatic route and beyond 49 percent and up to 74 percent is under the government approval route. An example of the government approval route would be foreign investment in digital media. Digital media does not qualify under the automatic route and will, at the very least, require approval of the Ministry of Information and Broadcasting. The processing time for applications under the standard operating procedure is 12-14 weeks. However, as a practical matter, this could take longer.

Accordingly, as a preliminary matter, a potential investor needs to determine the route and the sectoral limit of their proposed investment.

Registration as a foreign portfolio investor

Private equity investors could seek registration with the Securities Exchange of India (SEBI) as an FPI governed by the Indian SEBI (Foreign Portfolio Investors) Regulations, 2019 ("FPI Regulations"). The FPI concept was established to permit investments into Indian public market securities by foreign investors. In this respect, an FPI is essentially limited to investing in certain securities, including securities of companies listed or to be listed on a recognized stock exchange in India, domestic mutual funds in India - whether listed on a recognized stock exchange in India or not - and certain types of debt and government securities.

The FPI registration provides some advantages over the foreign direct investment route, as an FPI has the flexibility to buy and sell securities at prevailing market prices, without obtaining prior regulatory approval subject to the investment limits. Additionally, registered FPIs can invest in non-convertible debt securities issued by a listed Indian company (subject to investment threshold) whereas a foreign investor is otherwise permitted to invest in debt instruments issued by, or grant financing to, an Indian entity by complying with the 'External Commercial Borrowing' framework which entails significantly more stringent compliance and eligibility requirements.

However, FPIs are restricted in respect to the percentage of equity of an Indian company that they may own. There being a lower threshold of ownership in case of FPI compared to FDI, typically the FPI route will be used for making shorter-term financial investments rather than strategic long-term investments. The principal criteria for qualifying as a FPI are that the entity seeking registration must be appropriately regulated by a foreign regulatory authority and the entity must have sufficient experience, a good operating track record and a generally good reputation of fairness and integrity.

Registration as a foreign venture capital investor

A foreign investor could also seek registration with SEBI as a foreign venture capital investor ("FVCI") for the purpose of investing in private Indian companies. India has a vibrant start-up ecosystem, home to the third highest number of unicorns globally. The FVCI regime was introduced to encourage foreign investment into venture capital undertakings. FVCIs may invest in startups irrespective of the sector or in certain prescribed sectors including infrastructure, biotechnology and IT related to hardware and software. This would typically be done through a wholly-owned subsidiary of an offshore entity because of the potential for Indian tax liability for investors in an offshore entity making the investment in India.

In examining the application for registration as an FVCI, SEBI would generally look at whether the applicant is "fit and proper". This process involves examining the applicant's track record in the industry, its financial soundness, whether it is regulated by a foreign regulatory authority, etc. FVCIs registered with SEBI are also permitted to obtain registration as an FPI, subject to fulfilment of certain conditions including segregation of funds for investment under FVCI and FPI routes.

The FVCI route offers a number of benefits: an exemption from the pricing guidelines prescribed by the Indian foreign investment regulations which regulate the pricing for the purchase and sale of Indian securities; an exemption from a statutory six months lock-up which would otherwise apply to a foreign investor in the event of an IPO of their investee company in India; and an exemption from certain tender offer provisions in respect of the transfer of shares in an Indian company by the FVCI.

However, a number of restrictions are imposed on an FVCI, including a requirement to invest two-thirds of its 'investible funds' in unlisted equity or equity linked instruments and a prohibition from buying securities in the Indian public market, although an FVCI is permitted to subscribe to IPOs of Indian companies as a result of being classified as a qualified institutional buyer under SEBI regulations.

Conclusion

Projections indicate that India is poised to surpass Japan and Germany, positioning itself as the world's third-largest economy by 2027 which is underpinned by favourable fundamentals. This puts India in a position to have greater economic influence across the Asia-Pacific Region in the coming years. Private equity investments in India are expected to remain significant, reflecting investor confidence in the Indian economy. In making private equity investments into India, Canadian investors will need to be mindful of not only the applicable foreign investment restrictions in India, but also the optimal structure if they wish to establish to facilitate these investments.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.

We operate a free-to-view policy, asking only that you register in order to read all of our content. Please login or register to view the rest of this article.