Michael Bacina, Steven Pettigrove, Tim Masters, Jake Huang, Luke Higgins & Luke Misthos of the Piper Alderman Blockchain Group bring you the latest legal, regulatory and project updates in Blockchain and Digital Law.

Federal Court: Block Earner dodges the chopping block and ASIC criticised for misleading media release

In a closely anticipated decision, the Federal Court has absolved Block Earner from civil penalties arising from their centralised yield product, Earner, being found to be an unlicensed financial product.

ASIC commenced proceedings against Block Earner in November 2022 despite the Earner product already having been withdrawn, alleging that both the Earner and Access products (the latter being a DeFi pass-through yield product) were financial products offered without an Australian Financial Services Licence (AFSL). On 9 February 2024, the Federal Court ruled that the Access product was not a financial product, but the Earner product was, so between March and November 2022, Block Earner had offered unlicensed financial services and operated an unregistered managed investment scheme, being the Earner product. The parties were invited to make submissions on an appropriate penalty. ASIC sought $350,000 and Block Earner argued that it should be relieved from penalties by virtue of section 1317S of the Corporations Act 2001 (Cth) and in the alternative argued the penalty should be $60,000.

Section 1317S operates as a "safety net" for honest mistakes. If a person/entity contravenes a civil penalty provision of the Corporations Act, but is found to have acted honestly and fairly in the circumstances, a court has the power to excuse them from a penalty, despite there being a finding that the Corporations Act had been breached. This includes officers or employees of corporations who may have contravened rules but acted in good faith in doing so. This section operates similarly to section 183 of the National Consumer Credit Protection Act 2009 (Cth) (NCCP Act), which applies to credit providers. Section 183 of the NCCP Act provides that if proceedings are brought against a person and it appears to the court that the person has contravened a civil penalty provision of the NCCP Act but acted honestly, then the court may relieve that person either wholly or partly from a pecuniary penalty.

Brother of Hugh Jackman, his Honour Justice Jackman's decision dated 4 June 2024 found that Block Earner had not been "careless or imprudent" to any degree as it made a genuine attempt to comply with the requirements of the Corporations Act, despite ASIC's contentions to the contrary (at [12]).

The Court noted that Block Earner had formed an "unchallenged view", after obtaining legal advice from a leading specialist law firm, that there was no identified risk that the Earner product would breach any laws or regulations (at [14]).

Block Earner submitted that it effectively did the best that it could in an uncertain regulatory environment (at [17]-[19]), and the Court highlighted an extract from a recent Australian Law Reform Commission report which called:

the legislation governing Australia's financial services industry is a tangled mess

Block Earner had received adverse media coverage as a result of the 9 February 2024 decision that had affected its legitimate and lawful business. In particular, his Honour accepted a complaint by Block Earner that a media release published by ASIC the same day as the judgment, titled "Court finds Block Earner crypto product needs financial services licence", was unfair and misleading for reasons including that Block Earner did not "need" an AFSL as at 9 February 2024 as the Earner product had been withdrawn.

Block Earner gave evidence that ASIC's media release, and the news articles that took inspiration from the release, would likely have "devastating business and reputational consequences" for Block Earner, and the title of this media release has since been changed to use the past tense (at [20]-[27]).

His Honour accepted that Block Earner's active participation in policy discussions with key industry participants and regulators concerning crypto-asset products supported a finding that Block Earner had sought to conduct its business in a lawful manner (at [29]).

Despite ASIC's contention that there was no evidence that legal advice prepared for Block Earner was actually relied upon by it or specifically drafted in relation to its Earner product, his Honour found there was an "obvious inference" for which the legal advice was obtained (at [33]).

His Honour rejected a submission from ASIC that granting Block Earner relief from liability would send a message to the industry that it need not rigorously evaluate whether their offerings are regulated financial products and that the uncertainty inherent in a lay person's understanding of the Corporations Act may give rise to a successful defence by virtue of honesty and misapplication of complex laws (at [35]).

Instead, his Honour found that the contrary was likely true, and that the complexity and uncertainty of this area of law:

heightens the imperative that such [businesses] obtain legal advice from experienced and competent lawyers before launching their products and services (at [35])

This follows the principle that a person or business who:

- understands there is legal uncertainty in their proposed course of conduct, and

- takes the time to obtain legal advice from a qualified person, and

- then genuinely concludes that there is no identified risk of breaching the law,

ought fairly to be excused from liability if such proposed conduct happens to be a breach of a civil penalty provision (at [39]).

Despite the importance of the provisions breached by Block Earner (at [43]), his Honour found that Block Earner should be relieved from liability for a pecuniary penalty, and even if he was to not grant relief, no penalty would have been ordered (at [47]).

His Honour also needed to set a costs order and, in finding that ASIC had essentially won half of it's initial claim and lost half of it's initial claim, the parties were ordered to bear their own costs up to the date of the decision in February. ASIC was then ordered to pay Block Earner's costs after 9 February (including for the penalty hearing) and his Honour again called out ASIC's misleading media release as a factor in that decision, but also that he would have ordered costs against ASIC even disregarding the media release.

While the decision will likely be seen as supportive of the crypto industry, and highlight ways in which projects can seek to protect themselves when operating in an uncertain environment, it is better to not be the subject of litigation in the first place. The intricate and evolving nature of financial services laws and their application, particularly when it comes to emerging technologies like blockchain gives room for an approach like Justice Jackman's decision to waive Block Earner's potentially significant penalties, despite acknowledging the severity of its contraventions. This underscores the importance of obtaining early legal advice from qualified, specialist crypto lawyers before launching products or businesses.

The case also highlights that even in an uncertain regulatory environment like Australia, businesses must make a genuine attempt to comply with the requirements of the Corporations Act. If a business obtains legal advice and genuinely conclude that there is no identified risk of breaching certain laws, it may be excused from heavy fines if such conduct happens to breach a civil penalty provision.

Dapper Labs calls time out on NBA Top Shot class action

Dapper Labs, the company that mints NBA top shots into non-fungible tokens (NFT) – called NBA Top Shots, has reached a settlement agreement to finally put an end to a 3-year-long investor class action, which alleged the company violated US federal securities laws.

NBA Top Shots NFTs were an instant hit when they were released during the NFT bull market in 2020, under a partnership between the NBA and Dapper Labs. The top four most valuable NFTs of this collection are all shots by LeBron James, with the most expensive clip reached a high of USD$230,000. Dapper Labs was also the creator of another hugely popular and valuable NFT collection called CryptoKitties.

Three years ago, a group of NBA Top Shots NFT purchasers brought a class action accusing that the company's NBA Top Shot was unregistered securities because, according to the investors, the value of the NFTs would increase with the popularity of the project as a whole. This was a curious argument as it would be thought to extend to most kinds of collectibles, which are not usually considered regulated products.

The purchasers also argued that Dapper Labs prevented them from cashing out the NFTs for "months on end", and did not allow the NBA Top Shots NFTs to be exchanged on third-party NFT platforms.

Dapper Labs denied the accusations. In a court filing, their lawyers argued that the NBA Top Shot NFTs are basically digital basketball cards, which are collectibles that have a market value.

This position has never been, and would seem unlikely to be, tested in court now that the parties have agreed on a settlement, which still needs to be approved by the Court. Under the deal Dapper Labs will pay the purchasers a total of USD$4million, in exchange for the plaintiffs to relinquish their claims that the NFTs are securities.

A spokesperson of Dapper Labs also said that they are planning on implementing a mandatory employee training program focused on:

compliance with federal securities laws and ethical marketing practices.

In addition, Dapper Labs has promised to give up control over its remaining FLOW token to Flow Foundation to ensure the decentralisation of the Flow blockchain and ecosystem.

No regulator has brought any case against Dapper Labs in relation to the Top Shot NFTs yet though in April this year, Fortune reported that the SEC had once launched an investigation into Dapper Labs but closed it in September 2023.

This settlement has nevertheless shows the lack and need of legal clarity surrounding the nature of NFTs and other crypto assets. The risks that NFTs could be categorised as financial products or securities, particularly if promoted in certain ways is still a very real one in an environment of regulation by enforcement.

Dapper Labs' CEO, Ghregozlou said that:

We are continuing to push for more overarching regulatory clarity to showcase that consumer NFTs are not financial products and, as such, should be regulated under well-established consumer protection regimes at the state level

It seems only legislation from parliament will make clear whether NFTs are consumer goods or financial product.

Presidential veto stirs up the crypto world

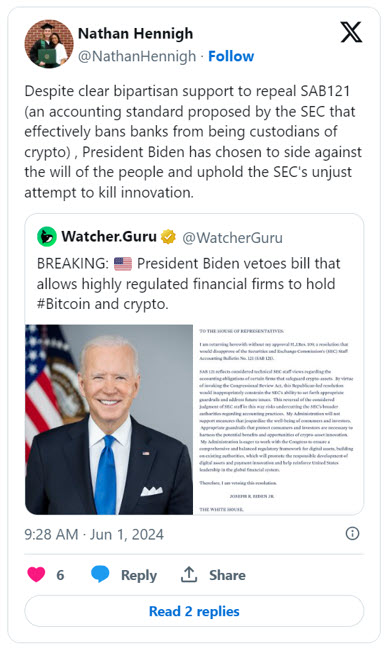

President Joe Biden has defended his decision to veto a resolution aimed at overturning the US Securities and Exchange Commission's (SEC) Staff Accounting Bulletin (SAB) No. 121. This controversial decision has drawn immediate criticism from the crypto community.

SAB121 was first issued by the SEC in March 2022, and required institutions that custody crypto-assets to record these holdings as assets and liabilities on their balance sheet. Critics argued that this requirement effectively prevented banks and other regulated entities from providing digital asset custody services at scale, and could deter banks from scaling a crypto business by imposing onerous capital requirements. SAB121 was also controversial as it treated crypto holdings differently from other custodied assets, which are traditionally held off-balance sheet. These factors combined led to significant pushback from the blockchain community, lawmakers and even the American Banking Association weighed in against SAB121.

The House of Representatives voted to repeal SAB121 by a vote of 228 to 182, passing the bill to the Senate. The Senate, mirroring the House's sentiment, voted to repeal SAB121 by a significant margin of 60-38 votes. Significant numbers of Democrats joined the Republican caucus to vote the measure through.

In his official letter dated 31 May 2024, President Biden emphasised his administration's commitment to consumer and investor protection, stating, "My Administration will not support measures that jeopardize the well-being of consumers and investors." The letter further explained the President's view that challenging the proposed guidelines of SAB121 would undermine the SEC's authority. He argued that reversing the SEC staff's considered judgment in this manner could potentially undercut the SEC's broader powers concerning accounting practices.

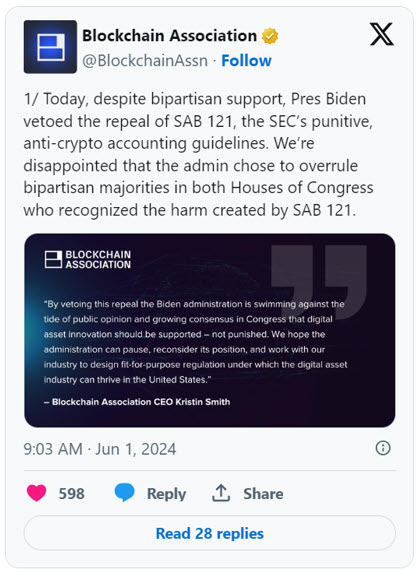

Following President Biden's veto, the Blockchain Association (a prominent crypto advocacy group) expressed its disappointment on 31 May via X, arguing that the administration's decision undermines the bipartisan consensus in Congress, which recognized the potential harm posed by SAB 121:

The wider crypto community also voiced their frustrations on social media, arguing that the decision stifles innovation and hampers the industry at a critical juncture.

Cody Carbone, the chief policy officer of the Digital Chamber, described the decision as a "slap in the face to innovation and financial freedom" in a 31 May X post.

This decision marks a significant moment in the ongoing dialogue between the crypto industry and regulatory authorities, especially in light of the potential impact the "crypto vote" will have on the upcoming US Presidential election. This latest event again highlights the need for a balanced approach that fosters innovation while ensuring consumer and investor protection.

SEC to cut check for USD$1.8M to Debt Box

The US Securities and Exchanges Commission (SEC) was recently sanctioned in a crypto enforcement matter, and has now been formally punished, being ordered to pay US$1.8M in legal and receivership fees.

In July 2023, the SEC obtained a freezing order against Digital Licensing (trading as Debt Box), and simultaneously sued the business, claiming that it was operating an illegal US$50M crypto scheme.

The SEC was successful in appointing a receiver over Debt Box's business at the time, effectively shutting down the business. The native token of Debt Box crashed by over 50 percent following the action.

However, Debt Box has continued to fight back, throwing a particularly devastating hook in leading evidence that the SEC had misled and lied to the Court when obtaining the initial injunction. That evidence led to the injunction and receivership ending in October 2023 and the SEC being asked to show cause why the SEC should not be sanctioned for their conduct. In March of 2024, the SEC was formally sanctioned for what the Court called:

acting in bad faith

and a

gross abuse of power

in obtaining the initial injunction. The SEC team acting on the case resigned after this decision and 6 Republican Senators wrote a letter to Gary Gensler, Chair of the SEC, calling the behaviour "unconscionable".

In the most recent decision, the SEC has been granted a motion dismissing the case without prejudice meaning that it can relitigate the matter. However, Debt Box was successful in obtaining a number of conditions which the SEC agreed to follow if the case is to be relitigated, including that the case must be refiled in the same court, presumably so the same Judge can oversee the matter.

The US$1.8M order includes $750,000 for receivership costs and $1M for legal costs, but nothing in damage for the business impact of the improperly gained restraining order, showing the very real outcomes for a Government agency which misleads the Courts, but that the damage from such actions leaves a continuing mark. There is no word at present as to whether the SEC will seek to relitigate the matter, as it remains under review.

The content of this article is intended to provide a general guide to the subject matter. Specialist advice should be sought about your specific circumstances.